This article has been reviewed by Sumeet Sinha, MBA (Emory University Goizueta Business School). Should you have any inquiries, please do not hesitate to contact at sumeet@finlightened.com.

What is Insurance and What Insurance Should I Buy?

Insurance is a very effective method of risk management and mitigation. Insurance is a contract between an individual or entity and an insurance company or a financial institution. You can protect yourself, with the right insurance, against unexpected financial losses that can be caused by multiple factors. We all like choices, but with so many options, what insurance plans should you buy? Let’s see an overview of the popular types of insurance available to make informed decisions on what insurance to buy and how much.

- What is Insurance? What Insurance Should I Buy?

- What are the Types of Insurance?

- Conclusion – Should You Get Insurance?

How do I Buy Insurance?

There are plenty of insurance companies out there that offer insurance products. Companies assess your risk profile and compute an insurance premium that you can pay any the insurance. You can buy insurance online directly from the company’s website. There are comparison websites where you can quickly compare features and premiums of multiple insurance policies at once.

You can also walk into an insurance company’s office, talk to a human agent and buy it from them, the traditional way.

What is Premium?

Premium, simply put, is the cost of buying the insurance policy (a contract that ‘insures’ or protects you) and keeping it in force. You can pay premiums paid monthly, annually, or sometimes even in a single payment for the entire duration of the policy, which could be multiple years.

The Premium can be determined on the basis of a few factors:

- Your Risk Profile i.e. how likely are you to file an insurance claim

- The Policy Limit or the maximum payout the insurance company will give in case of a claim made by you.

- Deductible or the threshold amount you are willing to cover before insurance company pays out a single dollar.

How do Insurance Companies Make Money?

Insurance is a numbers game. Companies that sell insurance want to sell the insurance policies to a lot of clients (persons or businesses). For each policy, the insurance company collects premiums. The basic math behind the insurance business is easy to understand. You collect premiums from the sale of all the insurance policies. You pay out money to clients for valid insurance claims. The amount you collect in premiums must be more than the amount you pay out in claims. Straight and Simple.

Now, Insurance Companies would like to make a decent margin on the premiums they collect. They factor the potential risk on their overall client base and determine the premiums accordingly. There is actuarial science (statistics) behind figuring out the risk profile of the clients to decide the premiums so that the ‘basic math’ explained above works out. That is not as easy as it seems.

Example of an Insurer Making a Profit

Let’s consider a Car Insurance Company. For simplicity, let’s consider just one type of car – say, Honda Civic. The premium for insuring a Civic against collision is $50 a month i.e. $600 a year. The Car Insurance Company has 10,000 clients, hence it collects $600 * 10,000 = $6,000,000 a year in premiums.

In case a Civic owner makes an insurance claim, the average cost to the insurance company is $5,000 (let’s assume this). Now, for the sake of simplification, in a year if there are less than $6,000,000 / $5,000 = 1,200 claims, the Insurance Company is making profits!

If there are only 1,000 claims in a year, the Car Insurance Company collects $6 Million in premiums, and pays out $5,000*10,000 = $5 Million in claims, hence making a profit of $6 Million – $5 Million = $1 Million!

How do I File an Insurance Claim?

Insurance products come with a set of terms and conditions. There are some cases and situations that may not be covered by an insurance product, so the buyer must ensure to read the terms carefully and ask clarifying questions before signing off on the contract.

If the need arises that you must file an insurance claim, it is best to contact the number provided (or your agent) by your insurance company for claims. Keep all your relevant documents i.e. policy number, an ID etc. You can explain your situation and ask them for assistance in processing your claim. If the insurance claim is deemed valid, please be aware that there might still be some ‘costs’ associated with the insurance claim, such as a deductible.

What is Deductible?

Let’s understand deductible with an example. You buy car insurance and are insured against collision damage. The car gets damaged in a collision, and according to the repair shop, would require $2500 for repairs. You contact the insurance company and provide all the details. The insurance company is ready to cover the cost of repair but reminds you that the policy comes with a $500 deductible.

‘What does that mean?’ you ask. The insurance guy explains, ‘this simply means that the insurance company will only pay the amount that exceeds the deductible. The $500 deductible is the threshold only above which the insurance would start paying for claims.’

Bestseller Personal Finance Books

So, in this case, the insurance company will pay out $2500 – $500 = $2000 to you for this claim.

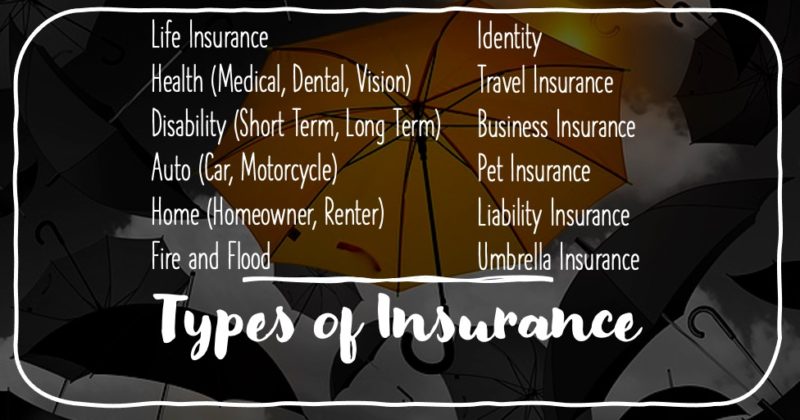

What are the Types of Insurance?

There are plenty of insurance products in the market and they keep bringing new products as demand evolves. You can find below the list of the most commonly known insurance products.

- Life Insurance

- Health Insurance (Medical, Dental, Vision)

- Disability Insurance (Short Term, Long Term)

- Auto Insurance (Car, Motorcycle)

- Home / Condo / Apartment Insurance (Homeowners, Renters)

- Fire and Flood Insurance

- Identity Insurance

- Travel Insurance

- Business Insurance

- Pet Insurance

- Liability Insurance

- Umbrella Insurance

This is not exhaustive and it is always a great idea to check whether insurance protection is available to suit your needs.

Life Insurance

Life Insurance is a financial risk mitigation contract that pays out money to beneficiaries in case of the death of the insured person. This way, the family (or other beneficiaries) left behind can have financial support. Mainly, there are two types of life insurance, one is Term Life Insurance and the other is Permanent Life Insurance.

The Term Life Insurance is the simpler version that covers you for a fixed period, say 5 or 10 or 20 or more years. It pays out the beneficiary (the person you nominate in the contract) in case of the death of the insured person.

Permanent Life Insurance, more expensive than term life insurance, has more features. It can also have an investment component built into it that grows over time.

While some prefer permanent life insurance, some prefer term life insurance and invest the difference in premium (permanent life insurance is costlier) separately.

Health Insurance

Depending on the country where you reside, health insurance can either be public or private or a mix of both. In the United States, most people get their health insurance through their employer. Typically an employer would buy health insurance from insurance companies such as United Healthcare, Aetna, Kaiser, Blue Cross, Humana, etc, and offer to pay a portion of the premium on behalf of the employee. For example, medical insurance that costs $800 a month can be covered 75% by the employer and 25% by the employee. So the employer would pay $600 a month, and the remaining $200 a month would come from the employee’s paycheck.

There are three main components of health insurance – Medical, Dental, and Vision. It’s always a good idea to evaluate whether you have appropriate coverage for all three components.

Long Term Disability Insurance

It covers essential expenses of the insured person in case of a long-term illness or a disability after an accident etc. Long Term Disability Insurance is generally provided through the employer and provides a percentage of the income to the employee while he or she is unable to work.

Some LTD Insurance plans also include incentives to help the employee get back to work.

Auto Insurance

Car owners can insure themselves and their cars against multiple risks. The following components mitigate risks for different possibilities.

Liability Insurance: to protect the other person, car, or property in case you cause an accident. Liability insurance is required by law, understandably, in most (if not all) regions of the world.

Collision: to pay for repairs in case you drive your car into an object such as a tree or a post, or lose traction and hit the side rail. You get the idea.

Comprehensive: to pay for incidents such as car theft, hail damage, or other damage that is not caused due to collision.

Uninsured Motorist Coverage: to pay for your medical bills when the other driver is at fault and causes an accident. Ideally, they should have liability insurance to cover you, but in case the other driver is uninsured, then uninsured motorist coverage protects you.

There are more coverage options with auto insurance, check with your insurance company for details and evaluate whether it is required for you in your case or not. For example, you might have a top of line medical insurance already, so adding on uninsured motorist coverage might be redundant.

For motorbike owners, there’s motorcycle insurance available as well.

Homeowners Insurance

Buying and owning a home is considered a matter of pride. Protecting your home and other assets inside the home is important. Homeowners’ insurance can protect the appliances, jewelry, electronics, musical instruments, etc against damages caused by theft, vandalism, some forces of nature, etc.

Every policy is different, so please make sure you read the fine print of what’s included and what’s not. For example, damages caused by the flood might not be covered in some homeowners’ policies, so you might want to consider getting flood insurance as an add-on.

Renters Insurance

When you rent a condo or an apartment, the landlord’s insurance does not cover your personal belongings. You can get renters insurance to insure your clothes, appliances, electronics, furniture, etc. against theft, vandalism, fire, etc. Some renter’s insurances also cover any damage caused by you to others’ property.

In case someone gets injured inside your rented apartment, your renters’ insurance can pay for their medical expenses too. As always read the fine print to understand what’s covered and what’s not covered by the policy.

Umbrella Insurance

The most organized people buy the appropriate insurance coverage for home and auto. However, sometimes there is a situation that falls through the crack and is covered by neither of the two insurance policies. Umbrella insurance can come in handy in such situations. Umbrella insurance can also protect you in case you are sued for an amount that exceeds your current policy’s payout limit.

Pet Insurance

We all love our dogs, cats, and other pets. They are family members and they deserve the best treatment in case of any illness or accident. Pet insurance helps pet owners with the vet bills in case an unfortunate situation arises where the pet needs medical attention.

Pet insurance covers diagnoses as well as treatments, in most cases.

Identity Theft Protection

Identity theft can cause serious damage to a person’s ability to secure a mortgage or a car loan. What if someone uses your social security number to do fraudulent activities? Besides being stressful, it can be an expensive process to reclaim your identity and repair the credit reports.

Identity Theft Insurance can help cover some costs such as legal fees, lost wages, childcare costs, phone bills, credit reports, etc. associated with the process of reclaiming your identity.

Business Insurance

Business owners need to protect themselves and their businesses from unwanted incidents too. While getting insurance coverage on equipment and furniture belonging to the business seems obvious, business owners must also consider getting covered for liability.

If the business has employees, Worker’s Compensation is required as well to cover their wages and medical bills in case of accidents.

Medical professionals should consider getting Medical Malpractice Insurance to protect themselves against medical negligence lawsuits.

Event Specific Protection Plans

An average couple in the US spends over $30,000 on their wedding. Right from food to location to decor, everything is planned meticulously and needs to be perfect. However, sometimes unforeseen circumstances can cause a postponement or event cancellation, or even theft or vandalism or other unfortunate incidents at the venue.

To protect yourself from financial stress, wedding insurance can come in handy. Wedding insurance can reimburse you a portion of the financial damage caused to you.

Similar to wedding insurance, there are other event-specific insurance plans out there that you can explore.

Conclusion – Should You Get Insurance?

We, at FinPins, believe that Risk Management & Insurance is an important pin to be placed on your personal finance board. Getting insurance is a great way to buy peace of mind at a fraction of the cost. While it makes sense to get as much coverage as possible, you should evaluate whether you are overinsured i.e. you’re paying high premiums for coverage that is either redundant or will never be required. Balance is the key.

Did you know? Investors can use stock options to mitigate the risk to their capital

Read more

Popular Topics: Stocks, ETFs, Mutual Funds, Bitcoins, Alternative Investing, Dividends, Stock Options, Credit Cards

Posts by Category: Cash Flow | Credit Cards | Debt Management | General | Invest | Mini Blogs | Insurance & Risk Mgmt | Stock Market Today | Stock Options Trading | Technology

Useful Tools

Student Loan Payoff Calculator | Mortgage Payoff Calculator | CAGR Calculator | Reverse CAGR Calculator | NPV Calculator | IRR Calculator | SIP Calculator | Future Value of Annuity Calculator

Home | Blog

Our Financial Calculator Apps

Page Contents